Transparent Liquidity: Private Credit Contagion and the Rise of Institutional DeFi

MARCH 25, 2026 • 15 MIN READ

Stablewatch Memo #2:

Recent weeks provided a clear demonstration of how modern financial systems handle stress. When redemption requests hit 9.3% of outstanding shares, BlackRock gated its $26 billion HLEND fund, trapping investor capital behind a 5% quarterly cap. Meanwhile, onchain lending protocols processed over $51.7 billion in stablecoin volume that same month without interruption, serving tens of thousands of active borrowers at rates competitive with the very market now seizing up.

The trigger was AI. The same technology revolution driving the infrastructure financing boom discussed in our first memo is now disrupting the enterprise software companies that private credit has actively been financing. Multiple estimates now place the broader private credit market around $2 trillion, with BIS data documenting $500 billion in SaaS lending concentrated in a sector where stocks collapsed nearly 30% in four months. Borrowers facing sudden revenue compression struggled to service high-yielding debt, and the fragility of the asset class was exposed when every major semi-liquid fund hit its redemption cap simultaneously, culminating recently as Ares and Apollo blocked investors from accessing more than half of their requested capital.

What follows examines how this TradFi liquidity crisis connects to a parallel development: DeFi lending protocols maturing into institutional credit infrastructure. Visa and Allium data documents $670 billion in stablecoin loans originated across five years. Euler has pivoted to institutional credit infrastructure, integrating Securitize’s DS Protocol to enable risk-isolated RWA lending vaults with encoded compliance. Sky operates a diversified yield engine generating $338 million in annual revenue across over $11 billion in stablecoin supply. But Stani Kulechov's warning — that DeFi should not become Wall Street's exit liquidity — rings through this analysis. The same bridges connecting institutional capital to onchain lending could just as easily serve as exit routes for trapped fund managers

Structural Fragility in Private Credit

How Semi-Liquid Vehicles Remind of Pre-2008 Fragility

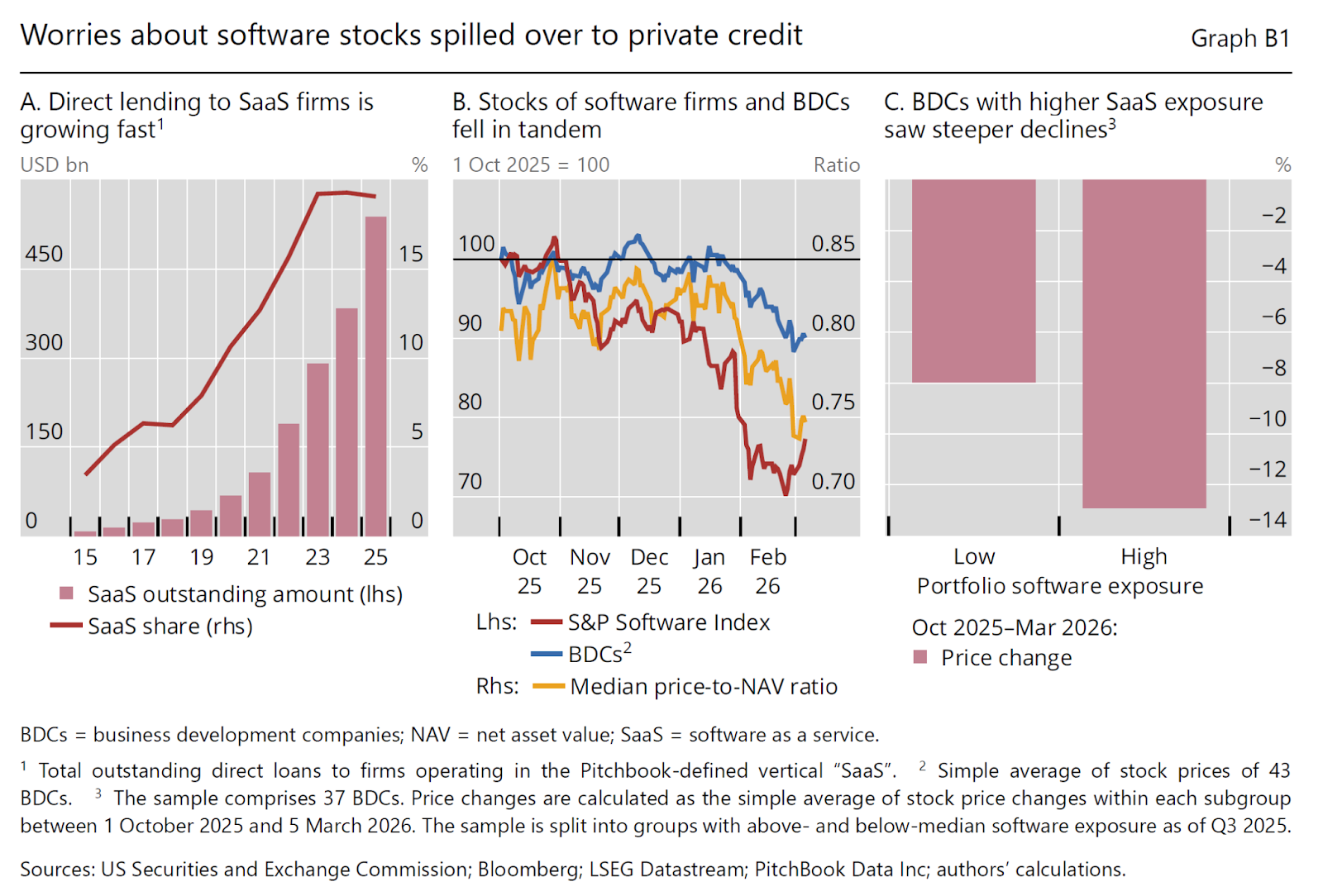

Various industry estimates now place the broader private credit market around $2 trillion, with the BIS March 2026 Quarterly Review documenting the scale of its exposure to AI disruption. Business development companies (BDCs), the retail-facing segment of that market, have grown into a significant channel for individual investor capital. Lending to private equity-backed software firms alone grew from $8 billion in 2015 to over $500 billion: 19% of total direct loans according to BIS data. Driven by margin compression in traditional institutional channels, alternative asset managers aggressively expanded retail distribution networks to capture new capital, transforming a once-niche credit structure into a significant pillar of the global shadow banking system.

The problem is straightforward. These vehicles fund corporate loans carrying four-to-seven-year durations with capital that investors can redeem quarterly — a mismatch that works only as long as withdrawal requests stay uncorrelated. When conditions deteriorate, correlations spike. Investors understand that liquid assets will be exhausted by the earliest redeemers, so even those with long-term horizons rush to withdraw. A credit concern becomes a self-fulfilling liquidity crisis.

At the start of 2026, market participants reached a sudden consensus that rapid AI advancements threatened the operational viability of legacy, private equity-backed software firms. The repricing was swift and broad: BIS data shows software company stocks collapsing by almost 30% between October 2025 and February 2026, dragging BDC stock prices down with them. Funds with heavier SaaS exposure fared worse, underperforming their peers. A third of private credit funds carry direct SaaS lending exposure, which meant the sector-specific shock translated almost immediately into an asset-class-wide repricing across institutional trading desks.

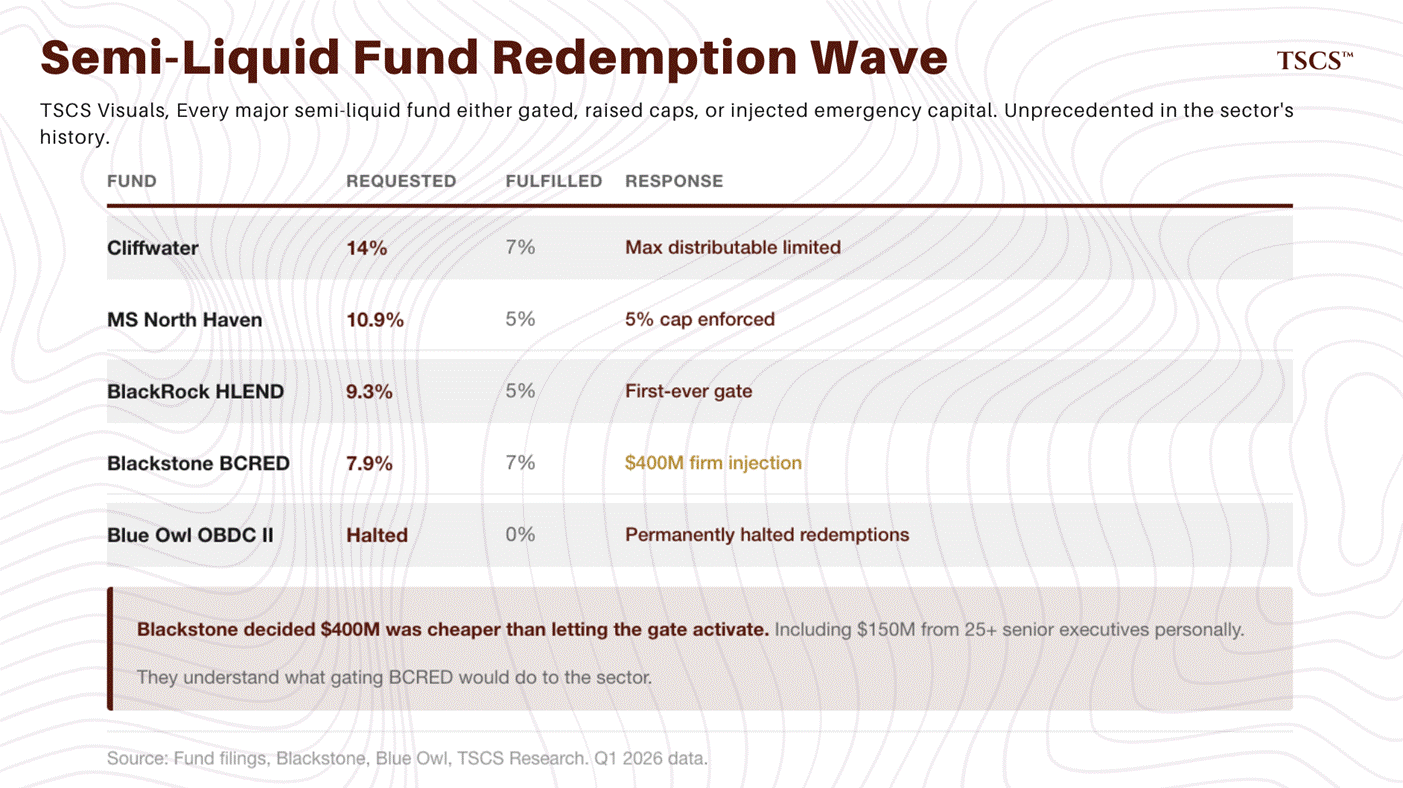

Meanwhile, retail investors sought exits in volume that overwhelmed available cash reserves. BlackRock's $26 billion HLEND fund became the headline case: redemption requests hit 9.3% of shares, and management capped withdrawals at 5% — the first major perpetual vehicle to enforce its gate since the stress began. The pattern repeated across the industry. Blackstone expanded its BCRED tender to 7% after absorbing $6.5 billion in requests against the $82 billion fund, with senior staff injecting $400 million of personal capital to shore up confidence. Cliffwater's $33 billion fund faced 14% redemption requests — double its quarterly cap — leaving half of requesting investors queued for the next window. Morgan Stanley's North Haven returned just 5% against 10.9% in requests. Liquidity provisions designed for uncorrelated withdrawals proved theoretical under correlated stress.

Underneath, credit deterioration was showing up in BDC income statements. Apollo MidCap Financial cut its quarterly dividend from $0.38 to $0.31 — an 18% reduction — as its portfolio default rate reached 5.8%. FS KKR Capital Corp had slashed its own dividend from $0.70 to $0.48, a 31% cut deeper than the company's own guidance, as non-accrual loans — debt where distressed borrowers have stopped making interest payments — climbed to 3.4% of its portfolio. These were not isolated markdowns but leading indicators of a trajectory that, according to Morgan Stanley, could push direct lending default rates to 8%. PIMCO's Christian Stracke offered the bluntest institutional assessment: "not just a crisis of confidence" but "a crisis of really bad underwriting." PIMCO's own shadow default rate for private credit sits at roughly 6%, well above the sub-2% rate in high yield, suggesting that official figures still undercount the damage.

Public markets delivered their own verdict on the managers behind these funds. Fortune documented $265 billion in alt-manager market cap destruction since September 2025. Blue Owl took the most extreme action of the cycle, permanently winding down its $1.6 billion OBDC II fund after a 200% surge in withdrawal requests and selling off roughly a third of its loan book.

Where there is distress, there is also opportunity for those positioned to bet against it — but private credit's opacity makes even that difficult. Goldman Sachs recently began pitching hedge funds on total return swap strategies to short corporate loans to PE-backed software companies. As the Financial Times reported, Goldman received a growing number of requests for these swaps, though at the time of reporting it had not executed any — because no counterparty was willing to take the other side.

In a telling development, Apollo itself announced plans to begin marking its private credit holdings daily — a radical departure from the quarterly valuations standard across the industry — even as CEO Marc Rowan warned of a coming shakeout and Apollo leadership conceded that industry-wide gating was “exactly the right decision” to manage the mismatch. The largest private credit manager conceding that quarterly marks are insufficient is an acknowledgment of the transparency problem that onchain architectures are ready to solve.

When Private Credit Ignores Public Market Distress

Glendon Capital Management — a $5 billion distressed debt fund founded by Oaktree veteran Holly Kim — argues that private credit lenders including Blue Owl were obscuring weaknesses in their portfolios and sitting on larger losses than reported. Glendon focused its criticism on Blue Owl's flagship $17 billion OBDC fund, where the lender had marked riskier junior slices of debt at values meaningfully above the public trading prices of safer, more senior debt issued by the same companies. In one example, OBDC marked $235 million in junior preferred stock and second-lien debt in HR software company Cornerstone OnDemand at approximately 90 cents on the dollar at year-end 2025 — while Cornerstone's most senior tranche of debt simultaneously traded at just 78 cents, a price broadly considered a sign of distress. Glendon identified similar disconnects across Blue Owl's loans to Barracuda, Peraton, and Conair Holdings, among others.

Financial logic demands that senior secured creditors must be made entirely whole before junior. By officially claiming that a junior tranche is worth 90 cents while the senior tranche trades at 78, asset managers are undermining the credibility of their entire internal valuation framework. Blue Owl argued the comparison was "apples to oranges" since marks were done at year-end 2025 while public loan prices had fallen sharply in early 2026 — but the broader pattern Glendon identified, of junior private marks exceeding senior public prices, was not confined to a single fund. Several other managers, including Ares and KKR, had debt funds with similar or higher marks on the same borrowers. Glendon further noted that yields on junior junk bonds, at less than 7%, were consistently cheaper than senior private credit loans yielding 10% or more — an inversion that suggests either public markets are dramatically mispricing risk, or private credit's promised returns embed credit deterioration that internal marks have not yet recognized.

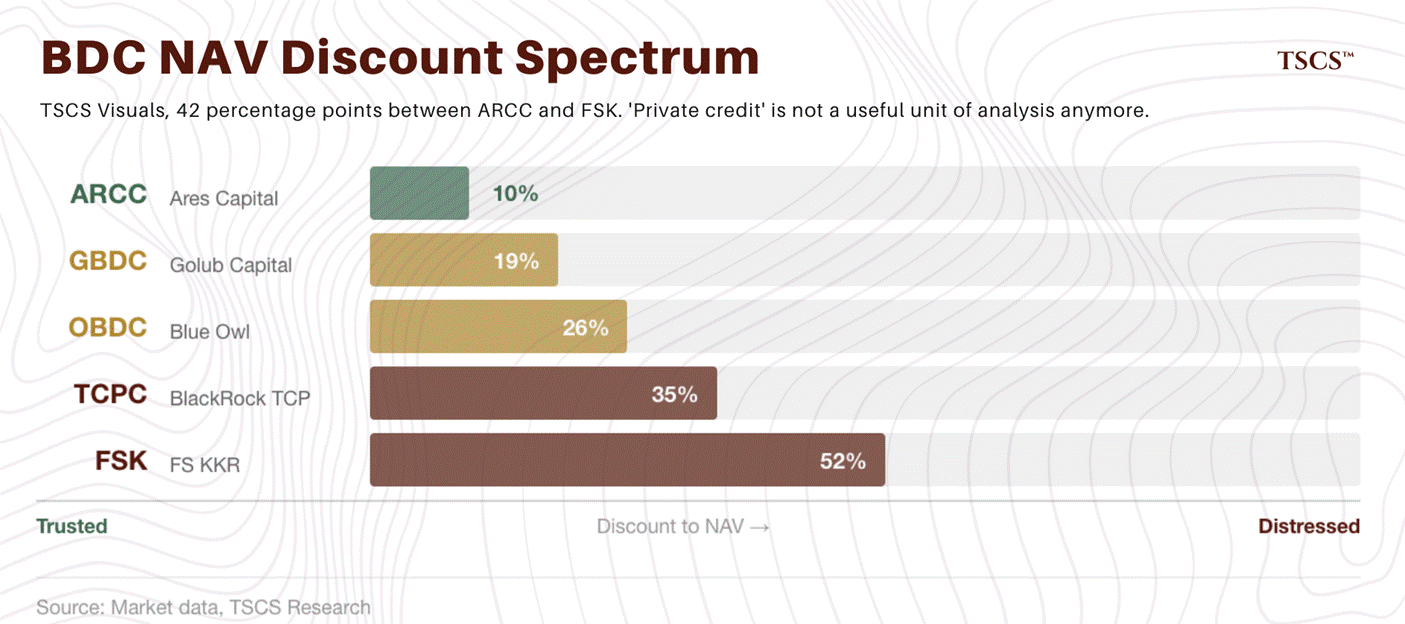

Secondary markets are pricing this skepticism in. OBDC's own share price implies a 25% discount to its reported net asset value, and Blue Owl's stock as manager has fallen more than 60% over the past year. Across the sector, public equity shares of major BDCs trade at an average 20% discount to stated net asset values — a broad rejection of the optimistic internal marks that alternative asset managers continue to publish. Discretionary gating and subjective accounting are failing to protect investors during correlated stress. Onchain credit infrastructure offers a structurally different model, one that could alleviate TradFi’s shortcomings.

Stablecoin Lending Reaches Institutional Scale

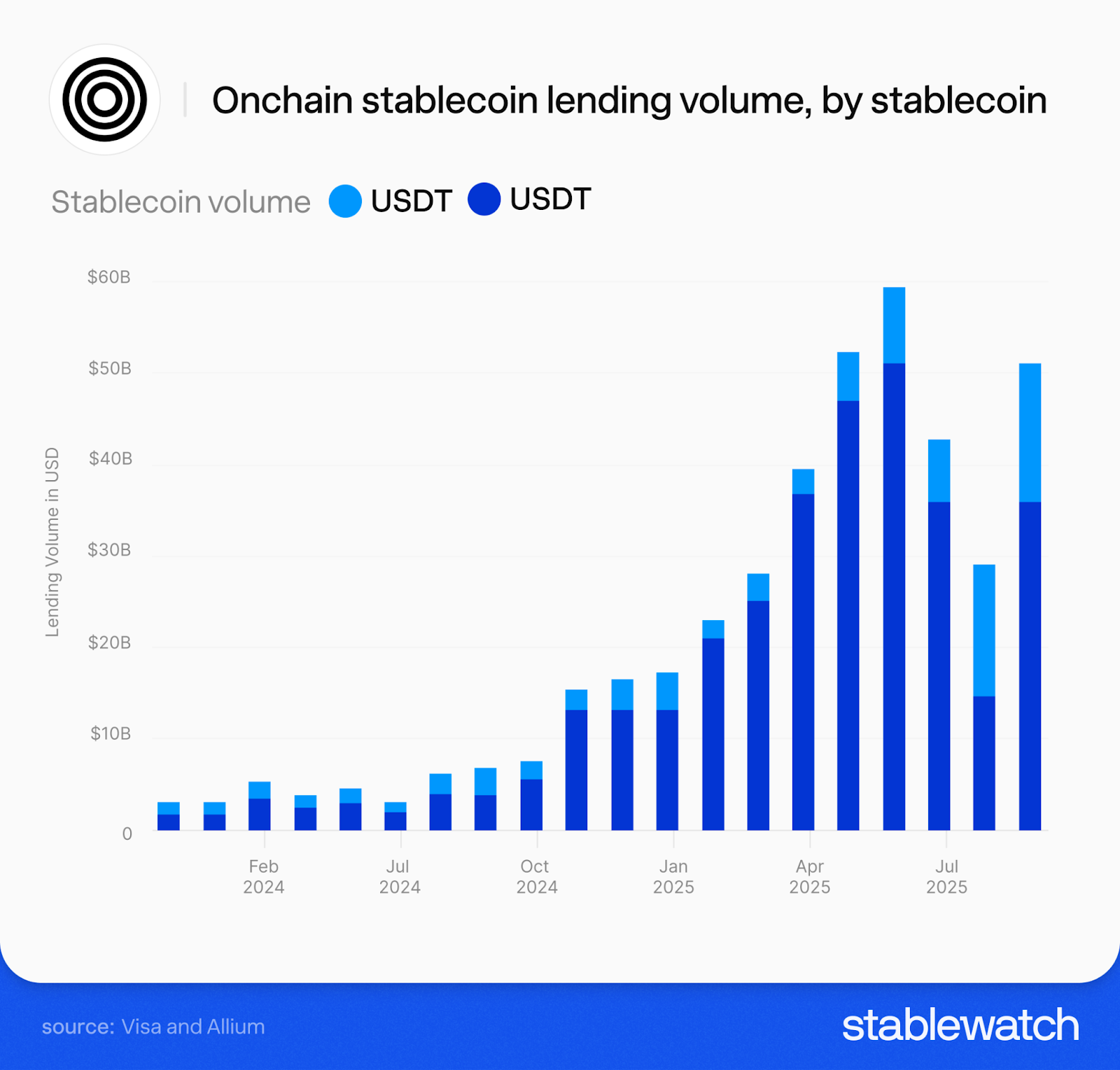

While private credit managers debate whether gating is a feature or a bug, a parallel lending market has been scaling without interruption. As traditional private debt funds unexpectedly restrict investor withdrawals, capital providers are increasingly driven to evaluate the deterministic, verifiable execution of onchain architectures. Joint research from Visa and Allium documents a stablecoin lending ecosystem that has originated over $670 billion in loans across five years, processing $51.7 billion in monthly volume as of August 2025, with $14.8 billion in active loans outstanding. An 84% utilization rate across $17.5 billion in deposited liquidity leaves little room to dismiss this as an experimental phenomenon.

Active stablecoin loans of $14.8 billion represent less than 1% of the roughly $2 trillion private credit market — a gap that shows both how much room onchain lending has left to grow and how far it remains from absorbing institutional flows of any systemic significance. Unlike the opaque BDC model, where internal marks hide duration mismatches, onchain credit protocols can be fully transparent: every loan, every piece of collateral, and every liquidation trigger. The structural advantages of onchain lending address the intermediation failures exposed by the current crisis, but they cannot cure underlying credit risk. Aave's founder Stani Kulechov has framed this tension directly: DeFi's institutional integration creates architecture for transparent, automated credit markets, but it simultaneously opens channels for distressed traditional assets to migrate onto new rails. Nothing in the architecture prevents distressed fund managers from using these channels to offload impaired assets onto onchain markets.

DeFi Offers An Alternative

Euler's Vault Kit Limits Contagion in Regulated RWA Markets

Euler Finance’s institutional pivot provides a technical solution to the semi-liquid BDC crisis. While traditional BDCs suffer from correlated stress — where a default in one sector like SaaS can force a fund-wide gate — Euler’s modular architecture replaces discretionary management with deterministic risk isolation. CEO Jonathan Han, formerly of Bridgewater Associates, has repositioned the protocol from a standard lending application into what the team calls "the credit layer for programmable finance”. Cumulative deposits have exceeded $4 billion across more than 10 chains, and the protocol has expanded its stack with EulerSwap and EulerEarn alongside its core lending markets.

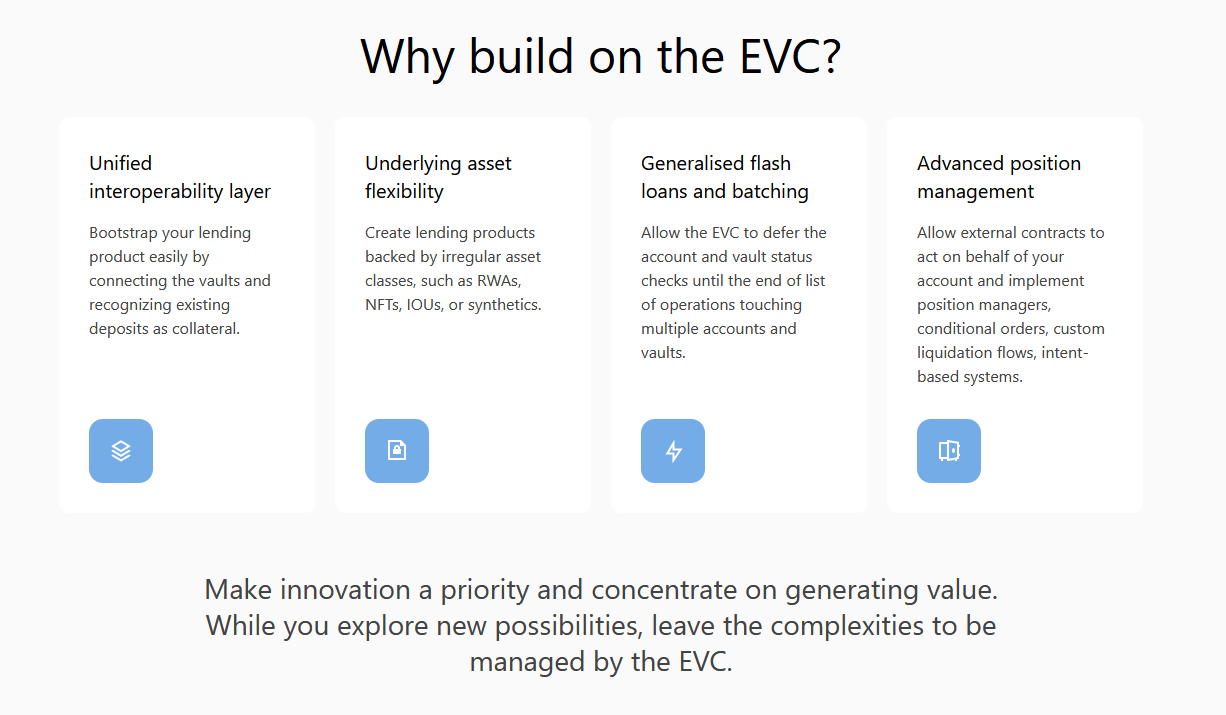

The core institutional play centers on the Euler Vault Kit (EVK) — infrastructure for deploying custom, risk-isolated credit markets. Rather than forcing allocators into generalized pools, the EVK lets asset managers set deterministic rules: who can supply capital, who can borrow, who can trigger liquidations. Bespoke credit agreements move from legal documentation onto smart contract architecture. If a tokenized private credit asset defaults, the damage is quarantined within its specific vault. Cross-collateralization with unrelated assets is prohibited by the architecture — a collapse in one specialized market cannot drain liquidity from separate, unrelated asset pools.

But isolation does not mean fragmentation. The Ethereum Vault Connector (EVC) allows permissioned institutional vaults to interface with shared open liquidity pools through standard interfaces. Bespoke credit markets can source external capital when necessary, participating in the broader DeFi ecosystem while maintaining the compartmentalization that prevents contagion from spreading.

Euler's integration of Securitize's DS Protocol demonstrates what this looks like in practice, solving the transparency problem that BDCs are scrambling to address only after the crash. Any asset issued through the DS Protocol standard can now serve as collateral without additional integrations. Custom vaults enforce KYC verification and execute regulatory transfer restrictions at the smart contract level, with liquidations restricted to verified addresses and Ultimate Beneficial Owner tracking built into the architecture. The compliance layer that traditional finance requires months of legal structuring to implement is encoded once and enforced automatically.

Sky's Agent Network Diversifying Yield

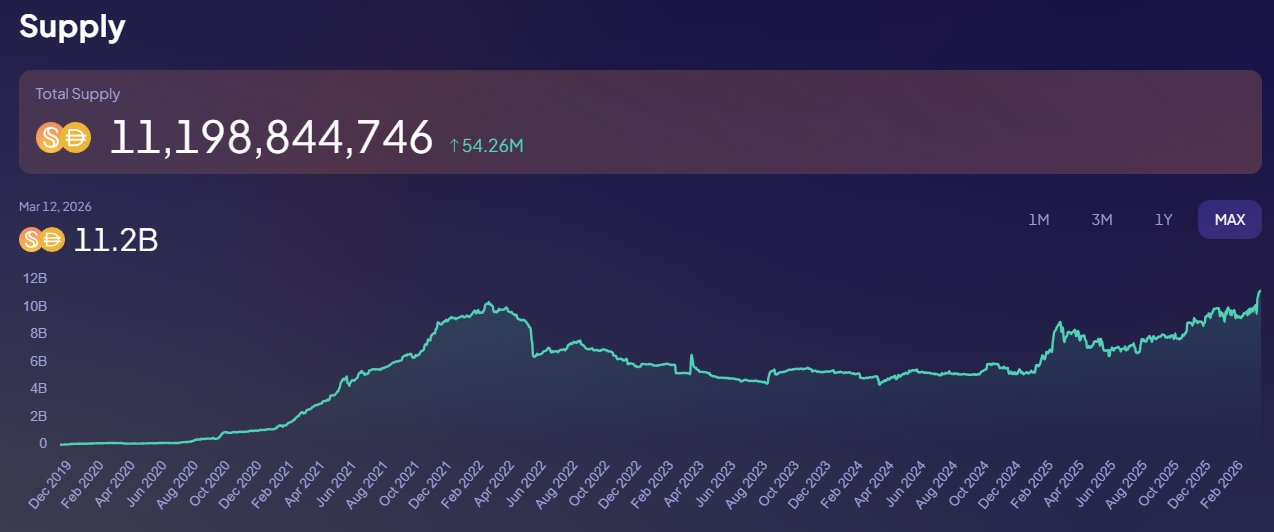

The vulnerabilities exposed by widespread BDC gating highlight a secondary, systemic flaw in traditional credit: allocation concentration risk. Sky (formerly MakerDAO) has built its architecture to address this via a decentralized agent model to enforce strict concentration limits and ecosystem-wide risk control. With over $11 billion in combined USDS and DAI circulating supply, $338 million in gross revenue during 2025, and the top revenue position among all protocols on Ethereum according to DefiLlama, Sky operates at a scale where its design choices carry real weight.

That scale has been expanding on multiple fronts. Sky's deployment of vaults on Morpho illustrates the speed advantage onchain architecture holds over traditional fund structures. The USDS Flagship Vault allocates 80% directly to the Sky Savings Rate with the remaining 20% diversified across stUSDS, cbBTC, wstETH, and ETH markets. Risk Capital Vaults offering higher-risk, higher-reward exposure in USDS, USDC, and USDT attracted roughly $74 million in deposits within 48 hours of launch. A dedicated USDT Savings Vault opened a new route for USDT holders to access SSR exposure — bringing the largest stablecoin by market cap into Sky's yield ecosystem for the first time, a development that signals broadening demand beyond USDS-native users.

Distribution is widening in parallel. Privy — a Stripe company powering almost 100 million wallets — integrated the Sky Savings Rate and sUSDS directly, giving millions of wallet holders native access to Sky's yield infrastructure without requiring them to navigate DeFi interfaces.

The core engine behind Sky’s resilience is the Sky Agent Network. Rather than relying on a monolithic treasury, the protocol contracts specialized, independent operators called Sky Agents to manage distinct yield strategies backing the USDS stablecoin. Spark operates primarily as the crypto capital markets arm, while its Spark Prime institutional lending suite channels over $9 billion in stablecoin liquidity toward institutional borrowers, drawing $150 million in early commitments from hedge funds at its February 2026 launch. Grove manages reserves of public credit and structured finance, including short-duration U.S. Treasuries, investment-grade debt and structured credit products. Obex targets capital intensive real-economy financing like AI compute and energy infrastructure. Keel extends the network distribution into Solana-native markets, including stablecoin lending and liquidity provision. The requirement of each Agent holding risk capital that serves as first line of defense against position deterioration, ensures that losses in one strategy are absorbed by the specific Agent’s buffer, preventing the USDS peg from the kind of repricing that destroyed $265 billion in alt-manager market capitalization. At the same time, concentration limits aim to prevent the kind of concentration risk materializing right now in the private credit markets.

A recent governance proposal allocated 70 million USDS in Genesis Capital to expand the network — 10 million for Keel, 25 million each for two new executor agents Amatsu and Ozone, and 10 million for an as-yet-unannounced Launch Agent 6. Rumored to facilitate broader sUSDS distribution and bridge diversified yield opportunities into retail-facing applications, Launch Agent 6 will scale Sky by connecting to institutional funds across a range of credit products.

Diversification across uncorrelated strategies is the core structural advantage, but managing multiple independent operators with distinct risk profiles introduces its own governance challenges. Correlation between supposedly uncorrelated strategies can surface under stress in ways that models often do not anticipate. The structure demands rigorous, continuous risk management not just at the individual agent level, but across the network, where aggregate exposure determines whether allocations remain sustainable.

Risks of Legacy Vulnerabilities

DeFi Becoming Wall Street’s Exit Liquidity?

Integrating traditional assets into onchain environments opens a direct contagion channel. The mechanisms driving this risk are economically straightforward. Fund managers trapped behind 5% quarterly redemption caps, burdened with portfolios of AI-disrupted software loans, have a clear incentive to tokenize these assets and access onchain liquidity. CoinDesk reported roughly $700 million in leveraged DeFi positions built against tokenized private credit products across major lending protocols — direct exposure to TradFi stress that did not exist a year ago.

The knowledge asymmetry compounds the risk. DeFi users carry strong intuition for onchain asset flows but often lack the tools to price complex duration, convexity, and fundamental credit risk embedded in traditional corporate debt. Sophisticated institutional actors can exploit this gap, marketing impaired assets as secure, high-yielding tokenized opportunities. Placing a loan on a blockchain does not repair the borrower's business model or improve recovery values in liquidation — it changes the venue where losses are realized, not the losses themselves.

Architecture as Risk Management

The protocols examined in this memo are not blind to these risks, their architectures are in large part, responses to them. Euler's vault isolation directly addresses the contagion vector. If tokenized private credit enters DeFi through a segregated EVK vault, its deterioration cannot drain liquidity from unrelated stablecoin markets. Sky's agent diversification addresses concentration risk from a different angle. Rather than allowing a single manager to deploy capital into distressed assets unchecked, the agent model distributes exposure across specialized, independently operated strategies with transparent, governance-controlled capital allocation. Underperformance is visible immediately, not buried in quarterly discretionary marks.

These remedies address the intermediation failures — the opacity, the gating, the marks — but they do not address the credit failures underneath. If the borrowers behind tokenized private credit are genuinely impaired by AI disruption, transparent liquidation of their collateral is still a loss. DeFi can make the loss visible and the process fair. It cannot make the losses smaller.

Transparency is Necessary but not Sufficient

Private credit's liquidity crisis is not a black swan. It is the predictable consequence of selling illiquid assets through semi-liquid retail vehicles while financing borrowers whose business models are being disrupted by the AI revolution whose financing we examined in Stablewatch Memo #1. With the market size of around $2 trillion, when BlackRock and Ares gate funds, when PIMCO calls it a "crisis of really bad underwriting”, and when Apollo fulfills only 45% of redemption requests — the demand for transparent, deterministic alternatives becomes more urgent than ever. The private credit contagion is not just a credit problem, but an architecture problem as well.

Stablecoin lending is no longer just an experiment, it is becoming an institutional-grade remedy for TradFi’s opacity. Euler offers regulated RWA collateral with encoded compliance and vault-level risk isolation — BlackRock's sBUIDL already operating through its architecture. Sky runs a diversified yield engine, proving that independent agents can generate hundreds of millions in revenue while actively defending against the concentration risk that is currently breaking traditional funds.

We have to, however, be mindful that this opportunity carries its own weight of risk. Active stablecoin loans still represent less than 1% of the private credit market. Euler's design is a promising architecture, not yet proven scale. Sky has size, but its Agent Network needs yet to prove its resilience. The onchain leveraged positions already building against tokenized private credit confirms that the contagion channel Stani warned about is an active risk vector. DeFi's transparent infrastructure could attract institutional capital seeking better architecture to scale on — or it could be pushed to absorb the distressed assets that TradFi markets can no longer contain. The stress test is coming.

Sources:

- Financial Times, Goldman pitches hedge funds on strategies to bet against corporate loans https://www.ft.com/content/52c4f129-891f-4afe-9cf4-3934630a50ad?syn-25a6b1a6=1

- https://www.bloomberg.com/opinion/articles/2026-02-20/private-credit-blue-owl-s-closed-fund-gates-raise-a-worrying-red-flag

- https://www.bloomberg.com/news/articles/2026-02-26/fs-kkr-private-credit-fund-cuts-dividend-amid-rise-in-bad-loans

- https://www.bloomberg.com/news/articles/2026-02-27/apollo-private-credit-fund-marks-down-portfolio-on-soured-loans

- https://www.bloomberg.com/news/articles/2026-03-02/blackstone-allows-investors-to-pull-record-7-9-from-bcred-fund

- https://www.bloomberg.com/news/articles/2026-03-06/pimco-says-private-debt-should-face-full-blown-default-cycle

- https://www.bloomberg.com/opinion/newsletters/2026-03-09/blackrock-guards-the-gates

- https://www.bloomberg.com/news/articles/2026-03-11/cliffwater-33-billion-private-credit-fund-redemptions-reach-14

- https://www.bloomberg.com/news/articles/2026-03-11/morgan-stanley-limits-redemptions-on-private-credit-fund-mmmlv7uj

- https://www.bloomberg.com/news/articles/2026-03-11/pimco-blames-sloppy-underwriting-for-private-credit-reckoning

- https://www.bloomberg.com/news/articles/2026-03-16/private-credit-default-rates-to-reach-8-morgan-stanley-says

- https://www.bloomberg.com/news/articles/2026-03-23/apollo-caps-private-credit-fund-withdrawals-as-requests-hit-11

- https://www.bloomberg.com/news/articles/2026-03-24/ares-limits-private-credit-fund-withdrawals-as-redemptions-surge

- https://www.advisorperspectives.com/articles/2026/03/12/apollo-mark-private-credit-daily

- https://www.ft.com/content/d0014b3a-94bf-4f78-8f47-64fca522e373

- https://fortune.com/2026/03/14/private-credit-meltdown-how-wall-streets-blackstone-kkr-apollo-ares-blue-owl-investment-craze-panic/

- https://tscsw.substack.com/p/private-credit-is-eating-itself

- https://www.bis.org/publ/qtrpdf/r_qt2603a.htm

- https://corporate.visa.com/content/dam/VCOM/corporate/solutions/documents/stablecoins-beyond-payments-onchain-lending-opportunity.pdf

- https://x.com/StaniKulechov/status/2030611384581423574

- https://www.coindesk.com/markets/2026/03/06/blackrock-private-credit-fund-is-latest-to-crack-hitting-crypto-prices-and-defi-markets

- https://x.com/0xJHan/status/2014754594253848955

- https://x.com/eulerfinance/status/2029977088284053515

- https://x.com/eulerfinance/status/2026760148065325264

- https://x.com/eulerfinance/status/2028883245685940264

- https://x.com/Securitize/status/2024484247440879944

- https://insights.skyeco.com/insights/sky-ecosystem-q4-update-and-2026-outlook-summary

- https://x.com/SkyEcoInsights/status/2031750834069934197

- https://x.com/SkyEcosystem/status/2026677223885869097

- https://x.com/SkyEcosystem/status/2029962047853563910

- https://x.com/SkyEcoInsights/status/2022314436447318232

- https://www.coindesk.com/business/2026/02/11/spark-looks-to-build-building-a-safe-bridge-between-onchain-capital-and-tradfi

- https://x.com/SkyEcosystem/status/2033187385215766649

Author

Piotr Kabaciński

Piotr is the Head of Research at Stablewatch, focused on in-depth market analysis and risk modeling for stablecoin yield products. He holds a PhD in Ultrafast Spectroscopy from Politecnico di Milano, and has coauthored over 15 high-impact papers in leading scientific journals. He has worked in DeFi as an investor for venture capital firms Geometry and Synergis Capital, after which he has founded a gas derivatives startup, later merged with Luban.

Piotr Kabaciński

Piotr is the Head of Research at Stablewatch, focused on in-depth market analysis and risk modeling for stablecoin yield products. He holds a PhD in Ultrafast Spectroscopy from Politecnico di Milano, and has coauthored over 15 high-impact papers in leading scientific journals. He has worked in DeFi as an investor for venture capital firms Geometry and Synergis Capital, after which he has founded a gas derivatives startup, later merged with Luban.